Notice

Recent Posts

Recent Comments

Link

| 일 | 월 | 화 | 수 | 목 | 금 | 토 |

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | ||||

| 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| 11 | 12 | 13 | 14 | 15 | 16 | 17 |

| 18 | 19 | 20 | 21 | 22 | 23 | 24 |

| 25 | 26 | 27 | 28 | 29 | 30 | 31 |

Tags

- 토익스피킹

- Programmers

- hackerrank

- Crawling

- lstm

- 프로그래머스

- Python

- 파이썬 주식

- SQL

- backtest

- 변동성돌파전략

- ADP

- PolynomialFeatures

- sarima

- docker

- 비트코인

- 데이터분석전문가

- randomforest

- 볼린저밴드

- 파이썬

- Quant

- GridSearchCV

- 백테스트

- 코딩테스트

- 빅데이터분석기사

- 실기

- 주식

- TimeSeries

- 데이터분석

- 파트5

Archives

- Today

- Total

데이터 공부를 기록하는 공간

백테스트 - MLP 본문

(참고) 파이썬을 활용한 알고리즘 트레이딩 6장

data = df.copy()

data['return'] = np.log(data['close']/data['close'].shift(1))

data.dropna(inplace=True)

data['direction'] = np.where(data['return']>0, 1, 0)

lags = 5

cols = []

for lag in range(1, lags+1):

col = "lag_{}".format(lag)

data[col] = data['return'].shift(lag)

cols.append(col)

data.dropna(inplace=True)

data

import tensorflow as tf

from keras.models import Sequential

from keras.layers import Dense

from keras.optimizers import Adam, RMSprop

optimizer = Adam(learning_rate=0.0001)

def set_seeds(seed=100):

#random.seed(seed)

np.random.seed(seed)

tf.random.set_seed(100)

set_seeds()

model = Sequential()

model.add(Dense(64, activation='relu',

input_shape=(lags,)))

model.add(Dense(64, activation='relu'))

model.add(Dense(1, activation='sigmoid'))

model.compile(optimizer=optimizer,

loss='binary_crossentropy',

metrics=['accuracy'])

cutoff = '2021-12-31'

training_data = data[data.index<cutoff].copy()

mu, std = training_data.mean(), training_data.std()

training_data_ = (training_data-mu)/std

test_data = data[data.index>=cutoff].copy()

test_data_ = (test_data-mu)/std%%time

model.fit(training_data_[cols], training_data['direction'],

epochs=20, verbose=False,

validation_split=0.2, shuffle=False)res = pd.DataFrame(model.history.history)

res[['accuracy','val_accuracy']].plot(figsize=(10,6), style='--')

model.evaluate(training_data_[cols], training_data['direction'])

cutoff_value = 0.5

pred = np.where(model.predict(training_data_[cols])>cutoff_value, 1,0)

pred[:30].flatten()

# 실제값

data['direction'].value_counts()

pred.flatten().sum()

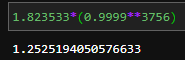

▶ 실제 19810중 3756 번 찾음

# long

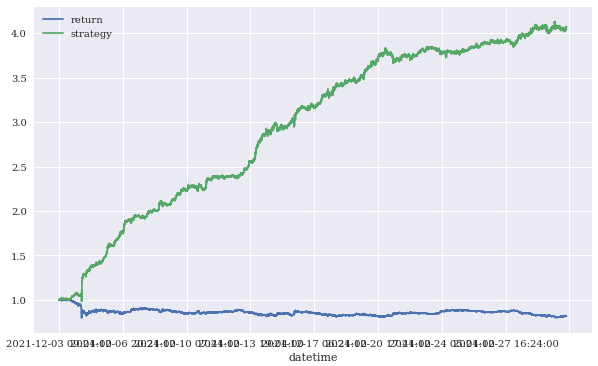

training_data['prediction'] = np.where(model.predict(training_data_[cols]) > 0, 1,0)

training_data['strategy'] = training_data['prediction']*training_data['return']

training_data[['return','strategy']].sum().apply(np.exp)

▶ 82% 수익률, 수수료 제외한 것이므로, 수수료 0.01%(0.005%*2, 매수 매도, 슬리피지 고려 x)로 가정시,

1.823533*(0.99990**3756) = 1.2525 > 25% 수익률로 감소 (3756번 매수/매도를 진행)

# long-short

training_data['prediction'] = np.where(model.predict(training_data_[cols]) > 0, 1,-1)

training_data['strategy'] = training_data['prediction']*training_data['return']

training_data[['return','strategy']].sum().apply(np.exp)

■ 다른 전략을 변수로 추가

data['momentum'] = data['return'].rolling(5).mean().shift(1)

data['volatility'] = data['return'].rolling(20).std().shift(1)

data['distance'] = (data['close']-data['close'].rolling(50).mean()).shift(1)

data.dropna(inplace=True)

cols.extend(['momentum','volatility','distance'])cutoff = '2021-12-31'

training_data = data[data.index<cutoff].copy()

mu, std = training_data.mean(), training_data.std()

training_data_ = (training_data-mu)/std

test_data = data[data.index>=cutoff].copy()

test_data_ = (test_data-mu)/std

set_seeds()

model = Sequential()

model.add(Dense(32, activation='relu',

input_shape=(len(cols),)))

model.add(Dense(32, activation='relu'))

model.add(Dense(1, activation='sigmoid'))

model.compile(optimizer=optimizer,

loss='binary_crossentropy',

metrics=['accuracy'])%%time

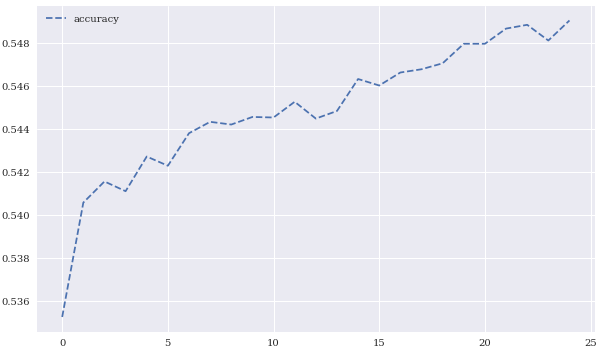

model.fit(training_data_[cols], training_data['direction'],

verbose=False,

epochs=25)res = pd.DataFrame(model.history.history)

res[['accuracy']].plot(figsize=(10,6), style='--')

cutoff_value = 0.5

pred = np.where(model.predict(training_data_[cols])>cutoff_value, 1,0)

pred[:30].flatten()

pred.sum()

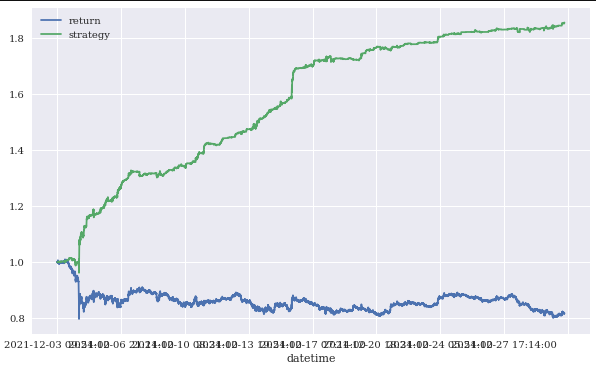

training_data['prediction'] = np.where(pred > 0, 1, 0)

training_data['strategy'] = (training_data['prediction']*

training_data['return'])

training_data[['return','strategy']].sum().apply(np.exp)

training_data[['return','strategy']].cumsum().apply(np.exp).plot(figsize=(10,6))

▶ MLP를 활용해서, 보다 좋은 결과를 얻을 수 있었으나, 이건 train data에 대한 결과일 뿐.

해야할 일

- 최적의 hypterparameter 최적화

- 모델 결과에 대해 cutoff_value 최적화

- 모델 평가지표에 accuracy 대신 정밀도(Precision)으로 평가해보기

* 정밀도 : 모델이 True라고 예측한 것중 실제로 True인 정도

* 재현율(recall) : 실제 True인데 모델이 True라고 예측한 정도

- 거래량을 조금 줄여야 할 것으로 보임 (슬리피지 및 수수료 때문에)

> 1분봉 대신 3분봉, 5분봉을 활용?

- 다른 지표와 연결을 추가적으로 함께 검토해야할 듯

'STOCK > 비트코인' 카테고리의 다른 글

| 백테스트 - MLP 5분봉 volume 변수추가 (0) | 2022.01.03 |

|---|---|

| 백테스트 - MLP 5분봉 (0) | 2022.01.03 |

| 백테스트 - logistic regression (0) | 2022.01.03 |

| 백테스트 - 모멘텀 (0) | 2022.01.02 |

| 업비트 API (0) | 2022.01.02 |

'STOCK/비트코인' Related Articles

more

Comments