STOCK/비트코인

Time Series Forecasing - one variable

BOTTLE6

2022. 2. 9. 22:35

2달 일봉데이터를 불러와서

TimeSeries 모델에 넣어서 돌려보기

1. Library & Data load

""" 시간대별 데이터 불러오기 """

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import pyupbit

from sklearn.metrics import mean_squared_error

from math import sqrt

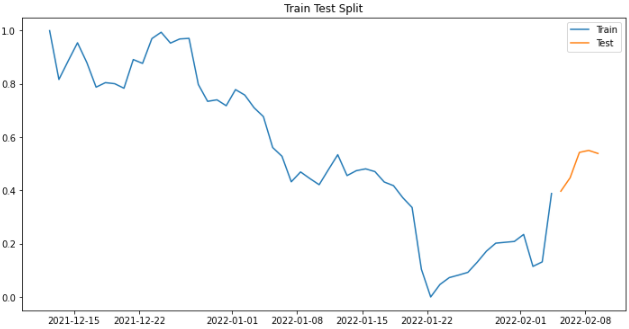

data = pyupbit.get_ohlcv("KRW-BTC", interval = "day", count=60)2. Train Test Split

dataset = data[['close']]

train_size=0.92

total_data = dataset.shape[0]

split = int((total_data * train_size))

train = dataset[0:split]

test = dataset[split:]

plt.figure(figsize=(12,6))

plt.plot(train.index, train.close, label='Train')

plt.plot(test.index, test.close, label='Test')

#plt.xticks(dataset.index, dataset.index, rotation='vertical')

plt.legend(loc='best')

plt.title("Train Test Split")

plt.show()3. MinMaxSclaing

from sklearn.preprocessing import MinMaxScaler

mm = MinMaxScaler()

mm.fit(train)

train = pd.DataFrame(mm.transform(train), columns=train.columns, index=list(train.index.values))

test = pd.DataFrame(mm.transform(test), columns=test.columns, index=list(test.index.values))

plt.figure(figsize=(12,6))

plt.plot(train.index, train.close, label='Train')

plt.plot(test.index, test.close, label='Test')

#plt.xticks(dataset.index, dataset.index, rotation='vertical')

plt.legend(loc='best')

plt.title("Train Test Split")

plt.show()

4. Modeling

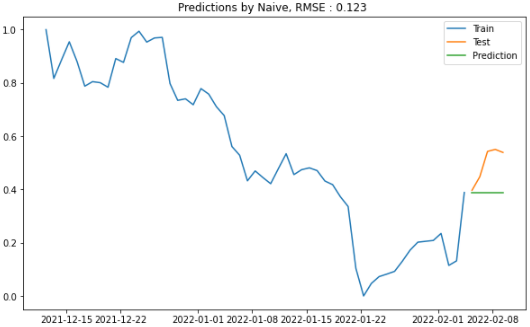

def plot_figure(title, pred, train_index=train.index, test_index=test.index, y_train=train.close, y_test=test.close):

rmse = sqrt(mean_squared_error(y_test, pred))

print(f"{title} Mean Square Error (RMSE): %.3f" % rmse)

plt.figure(figsize=(10,6))

plt.plot(train_index, y_train, label='Train')

plt.plot(test_index, y_test, label='Test')

plt.plot(test_index, pred, label='Prediction')

#plt.xticks(dataset["Month"], dataset["Month"], rotation='vertical')

plt.legend(loc='best')

plt.title(f"Predictions by {title}, RMSE : %.3f " %rmse)

plt.show()① Naive Approach

predictions_nv = test.copy()

# Copy the last observed Sales from training data

predictions_nv["Predictions"] = train.tail(1).iloc[0]["close"]

print (predictions_nv)

plot_figure(title = "Naive", pred=predictions_nv["Predictions"])

② AR (Auto Regressive)

from statsmodels.tsa.ar_model import AutoReg

model_ag = AutoReg(endog = train["close"], \

lags = 7, \

trend='c', \

seasonal = False, \

exog = None, \

hold_back = None, \

period = None, \

missing = 'none')

# endog: dependent variable, response variable or y (endogenous)

# exog: independent variable, explanatory variable or x (exogenous)

# lags: the no. of lags to include in the model

# [1, 4] will only include lags 1 and 4

# while lags=4 will include lags 1, 2, 3, and 4

# trend: trend to include in the model

# {‘n’, ‘c’, ‘t’, ‘ct’}

# ‘n’ - No trend.

# ‘c’ - Constant only.

# ‘t’ - Time trend only.

# ‘ct’ - Constant and time trend.

# seasonal: whether to include seasonal dummies in the model

fit_ag = model_ag.fit()

print("Coefficients:\n%s" % fit_ag.params)predictions = fit_ag.predict(start=len(train), \

end=len(train)+len(test)-1, \

dynamic=False)

predictions = pd.DataFrame(predictions, columns=['Predictions'])

predictions.index = test.index

result = pd.concat([test, predictions], axis=1)#.reindex(test.index)

plot_figure(title = "AR", pred=predictions['Predictions'])Coefficients:

intercept 0.012255

close.L1 1.198519

close.L2 -0.373919

close.L3 0.342944

close.L4 -0.348521

close.L5 0.083912

close.L6 0.019845

close.L7 0.037190

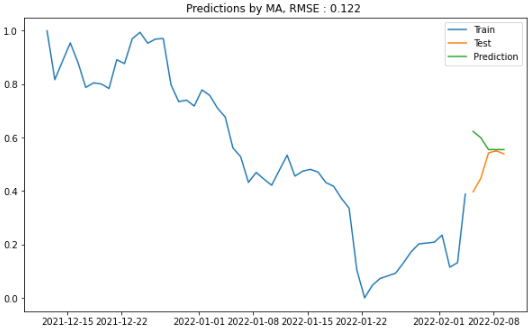

③ MA(Moving Average)

from statsmodels.tsa.arima.model import ARIMA

model_ma = ARIMA(endog = train["close"], \

order=(0, 0, 2))

# q = 2

# endog: dependent variable, response variable or y (endogenous)

# order: order of the model for the autoregressive,

# differences & moving average components.

fit_ma = model_ma.fit()

print("Coefficients:\n%s" % fit_ma.params)Coefficients:

const 0.555103

ma.L1 1.484815

ma.L2 0.821303

sigma2 0.013827predictions_ma = fit_ma.predict(start = len(train), \

end = len(train)+len(test)-1, \

dynamic = False)

plot_figure(title = "MA", pred=predictions_ma)

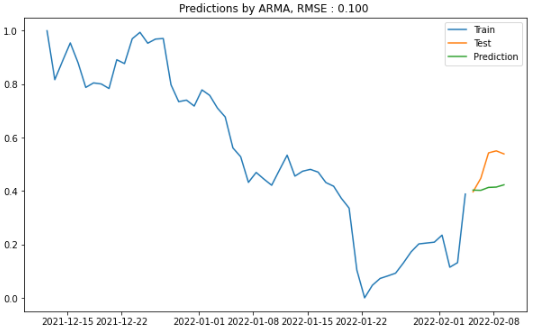

④ ARMA(Auto Regressive Moving Average)

from statsmodels.tsa.arima.model import ARIMA

model_arma = ARIMA(endog = train["close"], \

order = (2, 0, 1))

# endog: dependent variable, response variable or y (endogenous)

# order: order of the model for the autoregressive,

# differences & moving average components.

fit_arma = model_arma.fit()

print("Coefficients:\n%s" % fit_arma.params)Coefficients:

const 0.545970

ar.L1 0.170420

ar.L2 0.757241

ma.L1 0.855902

sigma2 0.005592

dtype: float64predictions_arma = fit_arma.predict(start = len(train), \

end = len(train)+len(test)-1, \

dynamic = False)

plot_figure(title = "ARMA", pred=predictions_arma)

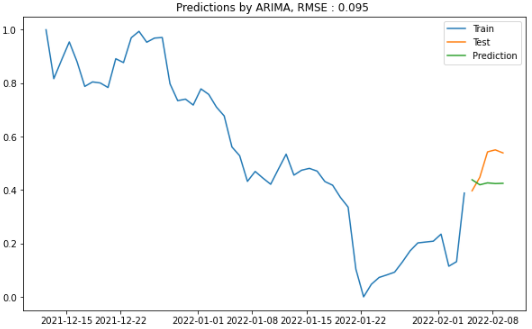

⑤ ARIMA(Auto Regressive Integrated Moving Average)

from statsmodels.tsa.arima.model import ARIMA

model_arima = ARIMA(endog = train["close"], \

order = (1, 1, 1))

# endog: dependent variable, response variable or y (endogenous)

# order: order of the model for the autoregressive,

# differences & moving average components.

fit_arima = model_arima.fit()

print("Coefficients:\n%s" % fit_arima.params)Coefficients:

ar.L1 -0.378863

ma.L1 0.638885

sigma2 0.005580predictions_arima = fit_arima.predict(start = len(train), \

end = len(train)+len(test)-1, \

dynamic = False)

plot_figure(title = "ARIMA", pred=predictions_arima)

⑥ SARIMA(Seasonal AutoRegressive Integrated Moving Average)

from statsmodels.tsa.statespace.sarimax import SARIMAX

model_sarima = SARIMAX(endog = train["close"], \

order = (1, 1, 1), \

seasonal_order=(0, 0, 0, 0))

# endog: dependent variable, response variable or y (endogenous)

# order: order of the model for the autoregressive,

# differences & moving average components.

# seasonal_order: (P,D,Q,s) order of the seasonal component of

# the model for the AR parameters, differences,

# MA parameters, and periodicity. s is the periodicity

# (number of periods in season), often it is 4 for

# quarterly data or 12 for monthly data (default, no

# seasonal effect).

fit_sarima = model_sarima.fit()

print("Coefficients:\n%s" % fit_sarima.params)Coefficients:

ar.L1 -0.378863

ma.L1 0.638885

sigma2 0.005580predictions_sarima = fit_sarima.predict(start = len(train), \

end = len(train)+len(test)-1, \

dynamic = False)

plot_figure(title = "SARIMA", pred=predictions_sarima)

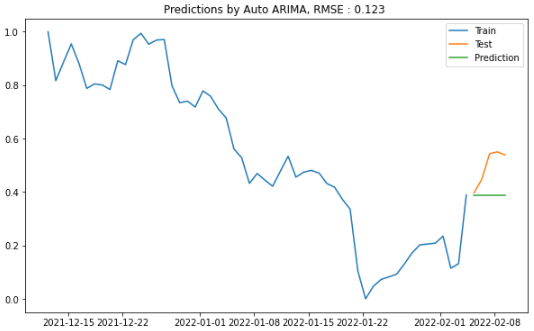

⑦Auto ARIMA

from pmdarima.arima import auto_arima

model_aarima = auto_arima (y = train["close"], \

seasonal=False, \

stepwise=True)

# seasonal : default=True, whether to fit

# a seasonal ARIMA.

# stepwise : default=True, the auto_arima

# function has two modes: stepwise

# & parallelized (slower)ARIMA(order=(0, 1, 0)predictions_aarima = model_aarima.predict(n_periods=test.shape[0], \

X=None, \

return_conf_int=False, \

alpha=0.05)

plot_figure(title = "Auto ARIMA", pred=predictions_aarima)

⑧ XGBOOST

dataXGB = dataset.copy()

# Restructure the data

dataXGB["Target"] = dataXGB.close.shift(-1)

# Drop the last null column because of shifting

dataXGB.dropna(inplace=True)

# Extract features & labels

X = dataXGB.loc[:,"close"].values

y = dataXGB.loc[:, "Target"].values

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = \

train_test_split(X, y, train_size = train_size, \

random_state = 0, shuffle=False)

import xgboost

reg = xgboost.XGBRegressor(objective='reg:squarederror', \

n_estimators=100)

reg.fit(X_train, y_train)predictions_xgb = reg.predict(X_test)

predictions_xgb = pd.DataFrame({'Predictions': \

predictions_xgb})

result_xgb = pd.concat( \

[dataXGB.tail(len(X_test)) \

.reset_index(drop=True), \

predictions_xgb], axis=1)

print (result_xgb)### 오류;;;

⑨ TBATS

from tbats import TBATS

# /databricks/python/bin/pip install tbats==1.1.0

model_tbats = TBATS(seasonal_periods=(12, 28),\

use_arma_errors=False,\

use_box_cox=False,\

n_jobs=None,\

use_trend=None,\

use_damped_trend=None)\

.fit(train.close)

predictions_tbats = model_tbats.forecast(steps=test.shape[0])

predictions_tbatsDF = pd.DataFrame()

predictions_tbatsDF["Predictions"] = predictions_tbats.tolist()

result_tbats = pd.concat([test.reset_index(drop=True), \

predictions_tbatsDF], axis=1)

print (result_tbats)

plot_figure(title = "TBATS", pred=predictions_tbatsDF["Predictions"])

⑩ ETS

from statsmodels.tsa.holtwinters import ExponentialSmoothing

model_es = ExponentialSmoothing(endog=train["close"], \

trend='add', \

seasonal='add', \

seasonal_periods=12, \

damped=True)

# Parameters

# endog : The time series to model.

# trend : Type of trend component (optional);

# options: "add", "mul", "additive",

# "multiplicative", None

# seasonal : Type of seasonal component (optional);

# options: "add", "mul", "additive",

# "multiplicative", None

# damped_trend : Should the trend component

# be damped (optional)fit_es = model_es.fit(optimized=True, \

use_boxcox=False, \

remove_bias=False)

predictions_es = fit_es.predict(start=test.index[0], \

end=test.index[-1])

predictions_es

plot_figure(title = "ETS", pred=predictions_es)

5. 예측력이 가장 좋은 모델이었던 TBATS로 예측해보기

steps = 5

history = mm.transform(dataset)

model_tbats = TBATS(seasonal_periods=(12, 28),\

use_arma_errors=False,\

use_box_cox=False,\

n_jobs=None,\

use_trend=None,\

use_damped_trend=None)\

.fit(history)

predictions_tbats = model_tbats.forecast(steps=steps)

predictions_tbatsDF = pd.DataFrame()

predictions_tbatsDF["Predictions"] = predictions_tbats.tolist()

predictions_tbatsDF["Predictions"]0 0.542856

1 0.485745

2 0.498366

3 0.505518

4 0.377700steps=5

delta = dataset.index[-1]-dataset.index[-2]

new_index = [ dataset.index[-1]+ delta*(i+1) for i in np.arange(steps)]

plot_figure(title = f"TBATS {steps}days", pred=predictions_tbatsDF["Predictions"], \

train_index = dataset.index, test_index=new_index, \

y_train=history, y_test=np.zeros(steps))

향후 5일간 하락할 것으로 예상

steps = 15

predictions_tbats = model_tbats.forecast(steps=steps)

predictions_tbatsDF = pd.DataFrame()

predictions_tbatsDF["Predictions"] = predictions_tbats.tolist()

predictions_tbatsDF["Predictions"]

delta = dataset.index[-1]-dataset.index[-2]

new_index = [ dataset.index[-1]+ delta*(i+1) for i in np.arange(steps)]

plot_figure(title = f"TBATS {steps}days", pred=predictions_tbatsDF["Predictions"], train_index = dataset.index, test_index=new_index, y_train=history, y_test=np.zeros(steps))

steps = 30

predictions_tbats = model_tbats.forecast(steps=steps)

predictions_tbatsDF = pd.DataFrame()

predictions_tbatsDF["Predictions"] = predictions_tbats.tolist()

predictions_tbatsDF["Predictions"]

delta = dataset.index[-1]-dataset.index[-2]

new_index = [ dataset.index[-1]+ delta*(i+1) for i in np.arange(steps)]

plot_figure(title = f"TBATS {steps}days", pred=predictions_tbatsDF["Predictions"], train_index = dataset.index, test_index=new_index, y_train=history, y_test=np.zeros(steps))

6. 데이터를 2달에서 3달로 변경

data = pyupbit.get_ohlcv("KRW-BTC", interval = "day", count=90)

dataset = data[['close']].copy()

mm = MinMaxScaler()

mm.fit(train)

dataset = pd.DataFrame(mm.transform(dataset), columns=dataset.columns, index=list(dataset.index.values))

plt.figure(figsize=(12,6))

plt.plot(dataset.index, dataset.close, label='Train')

#plt.xticks(dataset.index, dataset.index, rotation='vertical')

plt.legend(loc='best')

plt.title("Train Test Split")

plt.show()# 학습

history = dataset.copy()

model_tbats = TBATS(seasonal_periods=(12, 28),\

use_arma_errors=False,\

use_box_cox=False,\

n_jobs=None,\

use_trend=None,\

use_damped_trend=None)\

.fit(history)

steps = 5

predictions_tbats = model_tbats.forecast(steps=steps)

predictions_tbatsDF = pd.DataFrame()

predictions_tbatsDF["Predictions"] = predictions_tbats.tolist()

predictions_tbatsDF["Predictions"]

delta = dataset.index[-1]-dataset.index[-2]

new_index = [ dataset.index[-1]+ delta*(i+1) for i in np.arange(steps)]

plot_figure(title = f"TBATS {steps}days", pred=predictions_tbatsDF["Predictions"], train_index = dataset.index, test_index=new_index, y_train=history, y_test=np.zeros(steps))

steps = 15

predictions_tbats = model_tbats.forecast(steps=steps)

predictions_tbatsDF = pd.DataFrame()

predictions_tbatsDF["Predictions"] = predictions_tbats.tolist()

predictions_tbatsDF["Predictions"]

delta = dataset.index[-1]-dataset.index[-2]

new_index = [ dataset.index[-1]+ delta*(i+1) for i in np.arange(steps)]

plot_figure(title = f"TBATS {steps}days", pred=predictions_tbatsDF["Predictions"], train_index = dataset.index, test_index=new_index, y_train=history, y_test=np.zeros(steps))

steps = 30

predictions_tbats = model_tbats.forecast(steps=steps)

predictions_tbatsDF = pd.DataFrame()

predictions_tbatsDF["Predictions"] = predictions_tbats.tolist()

predictions_tbatsDF["Predictions"]

delta = dataset.index[-1]-dataset.index[-2]

new_index = [ dataset.index[-1]+ delta*(i+1) for i in np.arange(steps)]

plot_figure(title = f"TBATS {steps}days", pred=predictions_tbatsDF["Predictions"], train_index = dataset.index, test_index=new_index, y_train=history, y_test=np.zeros(steps))

7. 데이터를 2주일로 변경

(참고) https://cprosenjit.medium.com/10-time-series-forecasting-methods-we-should-know-291037d2e285

향후 계획

- 다변량 알고리즘 활용, 딥러닝 활용

- 여러 시계열 모델, 머신러닝 모델 결합해보기